You could be one phone call away from a significant financial upside in the form of a reduced tax bill.

For all the extra costs you have to cover when you’re in business to the active role you must pay in getting paid, being your own boss isn’t for everyone.

But there is one excellent financial reason to consider transitioning to a business structure if you qualify: Legal tax minimisation.

Before you get excited about the idea of paying no tax – a peculiarity of the Australian psyche – this is not about tax avoidance. Just so we’re 100% clear…

Want to join the family? Sign up to our Kidspot newsletter for more stories like this.

Do you qualify to be a business rather than a sole trader? Image: iStock

Do not attempt to avoid paying tax you legitimately owe!

You’ll eventually end up in hot water with the Australian Tax Office (ATO). It’s a serious enough offense that it’s sent people bankrupt before, or to jail.

But if you do qualify as a business and not just a sole trader, there could be a significant financial upside in the form of a reduced tax bill.

Here’s the theory:

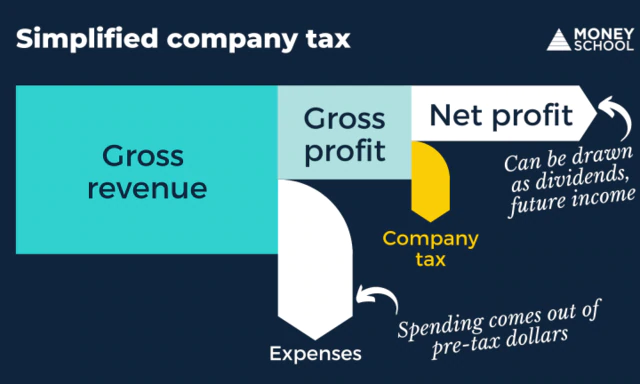

Income tax is paid on revenue. Company tax is paid on profit

When you’re an employee, you pay income tax on your salary.

Australia uses a marginal tax system, which means you pay a higher rate as you earn more.

The first $18,200 you earn in a year is tax-exempt – that’s called our tax free threshold – then the rates rise from 19% to 45% over a number of tax brackets.

If you were a business, this would be like paying tax on your revenue.

You earn an amount, pay the tax owed on it, then what’s leftover is yours to spend, save or invest as you please.

Company tax, however, has no tax-free threshold. It’s paid at a constant rate of 27.5 to 30%, depending on your company type and size (most small businesses would be in the 27.5% category).

But – and this is the kicker – you pay company tax on profit, not revenue.

What you spend to run the business, including your salary, is deducted before you pay company tax.

If that seems obtuse, let’s look at the numbers for financial year 2021 (or FY21, from 1 July 2020 to 30 June 2021):

Image: Money School

Example A: $60,000 a year via a salary

Someone earning $60,000 a year in salary can expect to pay $9,967 in tax, ignoring Medicare levies.

That means $50,033 hits their pocket after tax throughout the year. From that $50k, they pay all their expenses.

(Yes, they might reduce that tax through deductions such as work uniform laundering or a negatively geared property. But let’s keep it simple.)

Example B: $60,000 revenue via a company

Imagine they’ve used a company structure instead, earning $60,000 in revenue from clients.

By running their own business, they incur some legitimate expenses such as their phone and internet subscriptions, rent and power for the office, and some mileage on their car.

Say that amounts to $10,000 a year.

They might do something like:

- Pay themselves $45,000 as a salary, which incurs $5,092 in individual income tax.

- Deduct $10,000 from the remaining $15,000 income, leaving $5,000 profit.

- Pay 27.5% tax on that $5,000 profit, or $1,375.

The net result? The company structure means paying $6,467 in a combination of income and company tax.

That’s a neat $3,500 less tax than they’d pay as an employee.

In this case, the $3,625 after-tax profit could either be left in the company, ready to be drawn as dividends in a future tax year, or they could take it as salary and pay a bit more income tax.

Either way, you’re a few grand ahead versus giving it to the ATO. This is the difference between spending before-tax and after-tax dollars on expenses.

As you get into the higher tax brackets, it becomes more lucrative – a 27.5% company tax rate is much more attractive than the 45% you get in our top individual income tax bracket.

Also, for those who aren’t in a rush to access those profits, it’s a great way to spread income over many subsequent tax years without having to work harder. You just leave the profits in the company, having paid the 27.5% tax, then drip it out to yourself at $18,200 a year tax-free if you want to.

Image: Money School

Don’t skip the fine print

Before you head off to set up your business structure, a few reminders:

This only works if some of your usual after-tax spending could legitimately be deducted as a business expense. You can’t just deduct your entire internet bill if you use half of it streaming Netflix and your business doesn’t make money publishing Netflix show reviews. That’s a quick way to get a slap on the wrist from the ATO.

Running a business also adds complexity. At the very least, you’ll be submitting a quarterly Business Activity Statement as well as your personal income tax return. You may find your costs go up with business registration, bookkeeping support, insurance and other such running costs.

Finally, the ATO is excellent at closing loopholes. It won’t surprise me if changes are made to what qualifies as a business, and/or to the taxation rates that apply.

But for now: it’s a good way to keep more of the money you earn, in the right circumstances.

Lacey Filipich is the founder of Money School and Maker Kids Club, where she shares lots of ideas and tips on the whole family being smarter with their earnings.